Why 50% of Deals Miss Growth Targets

Revenue acceleration for private equity portfolios has become critical as nearly 50% of deals fail to meet growth expectations. Private equity is obsessed with AI. But AI isn't why portfolios miss growth targets.

Everyone is chasing AI in sourcing. AI in due diligence. AI in dashboards. Meanwhile, nearly 50% of GPs report they fail to meet growth expectations in more than half their deals.

At the same time, over 87% of PE professionals now say value creation is critical rising above 90% over the next five years. Commercial excellence and digital capability sit at the top of every priority list.

So the intent is clear. The execution is not.

The quiet killer isn't tooling. It's that the revenue foundation is broken on Day 1 post-close. And nobody fixes it fast enough.

The Real Problem Isn't AI—It's Alignment

Most portfolio companies grow to a certain size on founder energy, relationships, and hustle. Then the fund acquires them.

The thesis says "scale." The board says "accelerate."

But underneath?

Pricing has never been architected

ICP (Ideal Customer Profile) is loose

The offer isn't clearly positioned

Pipeline depends on two people

Conversion stages aren't measured properly

Sales is reactive, not structured

And now we're about to pour fuel on it.

If you scale demand into a broken revenue engine, you don't get growth. You get expensive noise.

Most growth misses aren't mysterious. They're structural. And often they're driven by misalignment between fund and management on what actually needs fixing first.

This is where a revenue accelerator for private equity becomes essential not as a consultant who gives advice, but as a partner who installs the commercial infrastructure that makes portfolio companies less dependent on founder hustle and more valuable to buyers.

Why Most Portfolio Companies Have Broken Revenue Engines

The average PE-backed business has grown on relationships and referrals. That got them to £5M, £10M, maybe £20M in revenue. But it won't get them to £50M. And it certainly won't get them to a successful exit at 5-10x EBITDA.

Here's what's typically broken at acquisition:

1. Pricing Leakage

Most businesses are leaving 20-40% of potential revenue on the table through underpricing, poor packaging, or lack of value-based pricing architecture. A revenue accelerator for private equity identifies these leaks in the first 30 days.

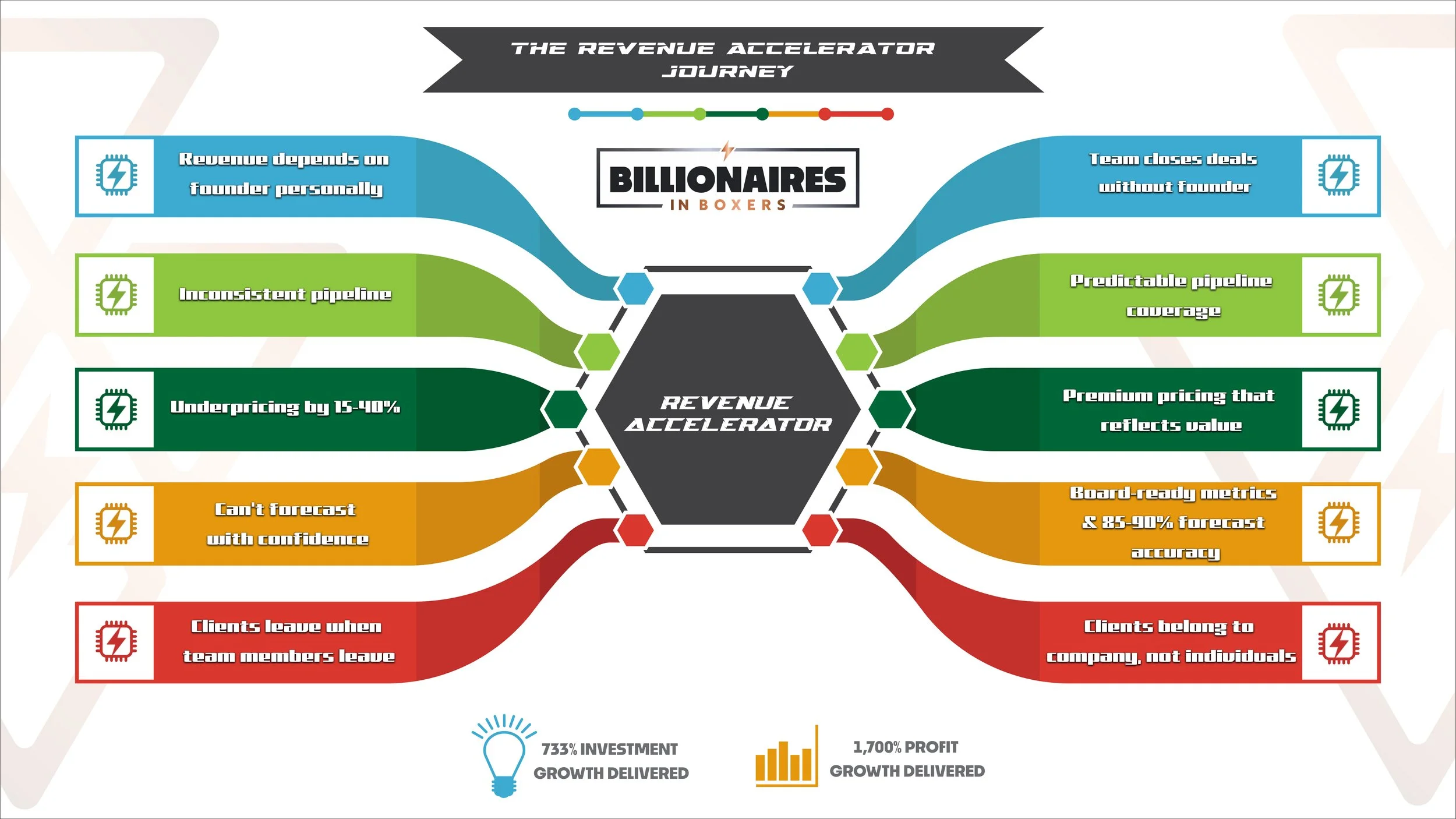

2. Founder Dependency

Revenue depends on the founder's personal relationships, energy, and sales ability. Remove the founder, and pipeline dries up. This is the single biggest risk to exit valuation.

3. Pipeline Fragility

There's no structured lead generation system. No nurture sequence. No predictable pipeline. Just hustle, hope, and referrals.

4. Poor Conversion Mechanics

Deals are won or lost based on relationship strength rather than a repeatable sales process. Nobody knows why some deals close and others don't.

5. Mispriced Offers

The business is either racing to the bottom on price or struggling to justify premium pricing because the offer isn't clearly differentiated.

These aren't growth problems. These are risk problems. And you can't scale on top of risk.

Revenue Accelerator Framework: The 3-Stage Sequence

Revenue acceleration isn't a campaign. It's a sequence. And it follows a strict order.

This is the same framework deployed inside OpenAI, Amazon, Microsoft, CBRE & Boeing, and across investment portfolios managing over $20Bn in assets under management. Now adapted specifically as a revenue accelerator for private equity portfolio companies.

Stage 1: Risk Removal—Before You Scale, Remove the Leaks

Before you chase upside, you remove downside.

You identify where revenue is leaking:

Margin erosion from poor pricing discipline

Founder dependency that creates exit risk

Pipeline fragility that makes revenue unpredictable

Poor qualification that wastes sales capacity

Broken handoffs between marketing and sales

Mispriced offers that leave money on the table

This is commercial due diligence after the deal. Most PE firms do financial and operational DD before close. But they rarely do revenue DD post-close.

That's a mistake.

Remove the reasons customers don't buy. Remove the reasons deals stall. Remove the reasons revenue disappears.

Most companies are losing 20–40% of potential revenue to structural issues they've never examined. That's not a growth problem. That's a risk problem.

And a revenue accelerator for private equity fixes it in Phase 1—before a single dollar is spent on scaling.

What Risk Removal Looks Like in Practice

Pricing audit: Identify underpriced offers, margin leakage, and packaging opportunities

Founder dependency assessment: Map where revenue relies on personal relationships

Pipeline health check: Audit lead sources, conversion rates, and sales process consistency

Offer clarity review: Ensure positioning is clear, differentiated, and defensible

Sales process documentation: Capture what's working (and what isn't) in the current approach

This phase typically takes 2-4 weeks and immediately surfaces 15-30% revenue opportunity that requires zero additional marketing spend.

Stage 2: Revenue Reactivation & Alignment

Now you align. This is where the revenue accelerator for private equity methodology installs the commercial engine:

Offer clarity: Package your services/products in a way that makes buying decisions easier

Pricing integrity: Architect pricing that reflects value, not competitor benchmarking

ICP discipline: Define and target the customers who buy fastest and pay most

Nurture architecture: Build automated systems that move prospects toward purchase

Conversion mechanics: Create repeatable sales processes that work without the founder

This is where growth actually starts. Not because you generated more leads. Because you made it easier for the right buyers to say yes.

This is where commercial excellence stops being a "sales enablement project" and becomes a board-level lever.

The Revenue Alignment Deliverables

A complete revenue accelerator for private equity engagement in Stage 2 delivers:

Structured sales process that any sales hire can execute

Pipeline management system with clear stages, conversion metrics, and forecasting

Pricing architecture that maximizes margin without sacrificing volume

Go-to-market strategy tailored to your ICP and competitive landscape

Outreach systems that generate qualified pipeline without founder involvement

Conversion frameworks that turn prospects into customers predictably

Stage 2 typically takes 2-6 months depending on business complexity. But the ROI is immediate: higher close rates, shorter sales cycles, and revenue that doesn't evaporate when the founder is out of the room.

Stage 3: Growth Strategy, Now You Go All In

Only now do you scale aggressively.

And yes—this is where AI becomes powerful. But not as a shortcut.

AI is a research tool. A growth tool. An efficiency tool.

It compresses learning curves. It identifies patterns across markets. It sharpens positioning. It coaches sales teams at scale. It accelerates diagnostics.

But AI cannot fix a broken foundation. It can only amplify what's already there.

If your fundamentals are weak, AI makes you faster at weak execution. If your fundamentals are strong, AI becomes a moat.

That's the difference.

How AI Enhances Revenue Acceleration (Stage 3 Only)

Once Stages 1 and 2 are complete, a revenue accelerator for private equity portfolio company can deploy AI to:

Market intelligence: Analyze competitor positioning, pricing, and messaging at scale

Sales coaching: Provide real-time feedback to sales teams using proven playbooks

Pipeline forecasting: Predict deal outcomes based on historical patterns

Content generation: Create outreach sequences, proposals, and follow-ups faster

Customer insights: Identify buying signals and engagement patterns

But none of this works if the foundation is broken. AI is Stage 3. Not Stage 1.

Why AI Without Foundation Is Expensive Noise

The market is obsessed with AI for good reason. It's transformative. But only when applied to solid fundamentals.

Here's what happens when PE firms skip Stages 1 and 2 and jump straight to AI-powered growth:

More leads, same conversion rate: AI floods the pipeline with unqualified prospects

Faster execution of broken processes: You scale inefficiency at higher cost

Founder dependency increases: AI can't replace the founder's personal selling ability

Margin pressure intensifies: Without pricing architecture, AI drives volume at the expense of profit

A revenue accelerator for private equity knows the sequence matters. Fix the foundation first. Then deploy AI to amplify what's working.

According to a Bain & Company study on PE value creation, the most successful portfolio companies focus on operational improvements and commercial excellence before technology deployment.

That's not a coincidence. That's the playbook.

Capital Should Be Talking About Revenue Architecture

The only defensible alpha left in this environment is operational value creation.

Multiple expansion is not a strategy. Commercial execution is.

And the first question post-close shouldn't be: "How do we scale?"

It should be: "Where are we leaking?"

If you're seeing good assets underperform on growth, it's rarely the market. It's almost always the revenue foundation. And that's fixable.

What a Revenue Accelerator for Private Equity Actually Delivers

When you engage a revenue accelerator for private equity like Billionaires in Boxers, you get:

Immediate risk identification: 15-30% revenue opportunity surfaced in 2-4 weeks

Structured sales infrastructure: Repeatable processes that work without the founder

Pricing optimization: Margin expansion without volume loss

Founder independence: A business that runs (and sells) without dependency on key individuals

Exit-ready valuation: 5-10x earnings multiples instead of 2-3x

This isn't theory. This is the same methodology deployed across $20Bn+ in portfolio assets. Now available to mid-market PE firms managing £500K to £50M revenue companies.

Final Thoughts: Revenue Acceleration Is a Sequence, Not a Sprint

The PE industry is waking up to a hard truth: you can't scale what's broken.

AI won't save you. More capital won't save you. Better dashboards won't save you.

What will save you is installing the commercial infrastructure that makes revenue predictable, scalable, and founder-independent.

That's what a revenue accelerator for private equity does. Not through advice. Through execution.

Remove the risks. Align the engine. Then scale.

In that order.

Happy to compare notes with any GP, Operating Partner, or portfolio leader dealing with this right now.

Ready to Fix Your Portfolio's Revenue Foundation?

If you're a GP, Operating Partner, or portfolio CEO watching good assets underperform on growth targets, the problem isn't mysterious. It's structural.

Book a call to get clarity on what's leaking, what's broken, and exactly where to start fixing it.

Book an Introductory Call | Learn More About Our Revenue Accelerator Methodology

About the Author

Phil Pelucha is a Portfolio Growth Partner and revenue acceleration strategist whose methodology has been deployed inside OpenAI, Amazon, Microsoft, CBRE & Boeing, and across investment portfolios managing over $20Bn in assets under management.

He is a New York Magazine 40 Under 40 honouree, Clutch US-ranked Top Global B2B Sales Influencer, and UK Business Awards Growth Consultant of the Year.

Phil built Billionaires in Boxers to make the same commercial strategies available to growth-stage businesses and PE portfolio companies that investment firms pay millions for.